Earlier this year I wrote an article asking, “Are digital editions dead?” The reason for the question stemmed from my confusion over why more publishers don’t offer branded digital editions of their print publications, and for those who do, why so many of them rarely market them. Instead of bundling them and promoting them, many publishers hide their digital replicas in the bowels of their websites.

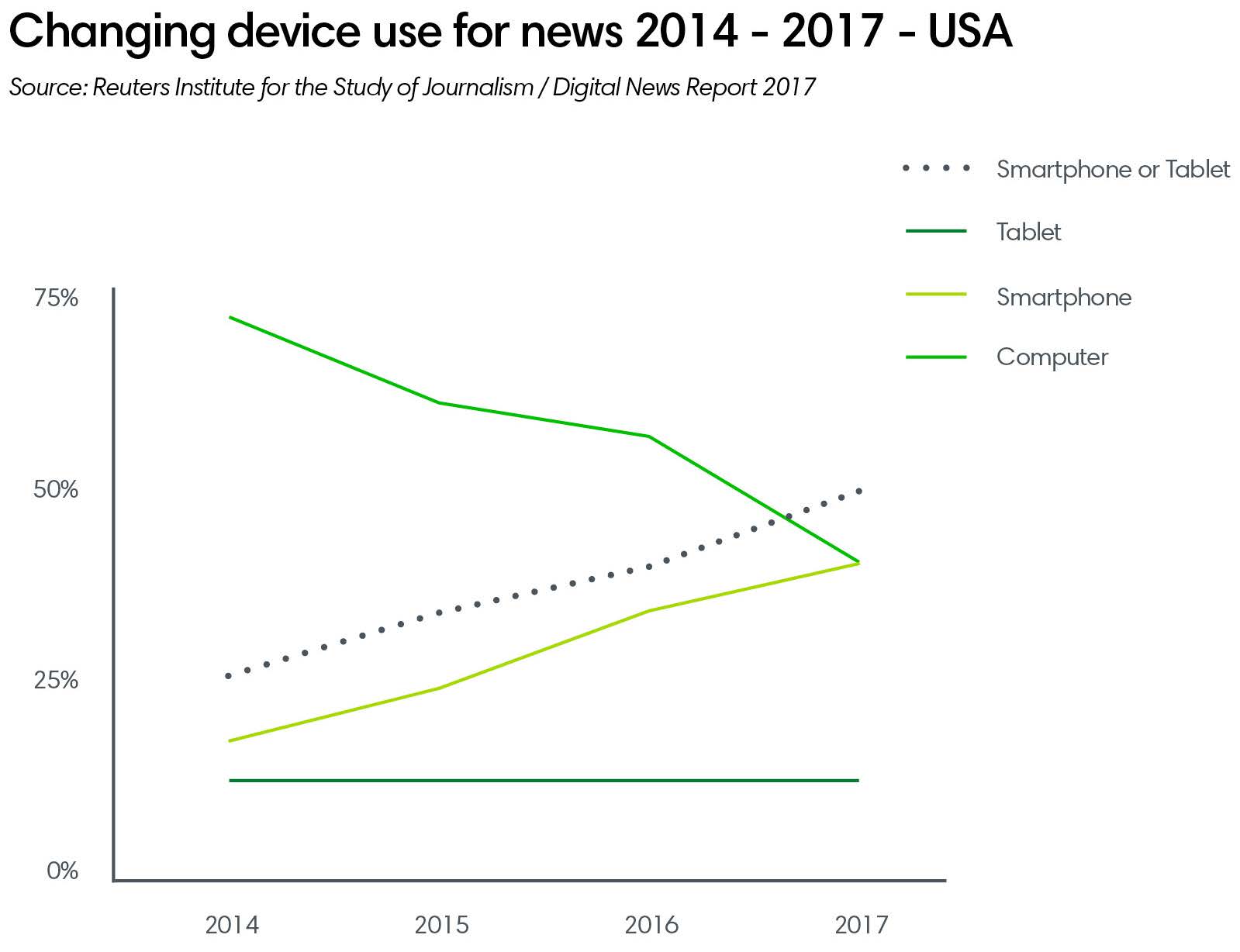

And then there are those publishers who restrict the platforms on which they offer digital editions, focusing on desktop and tablets, while ignoring the fastest growing market of all – smartphones.

Perhaps they’ll cannibalize their print revenue if they offer their branded edition across all platforms. Or maybe they support the claims by some pundits that no one wants to read digital editions anymore. Make no mistake. Nothing could be further from the truth.

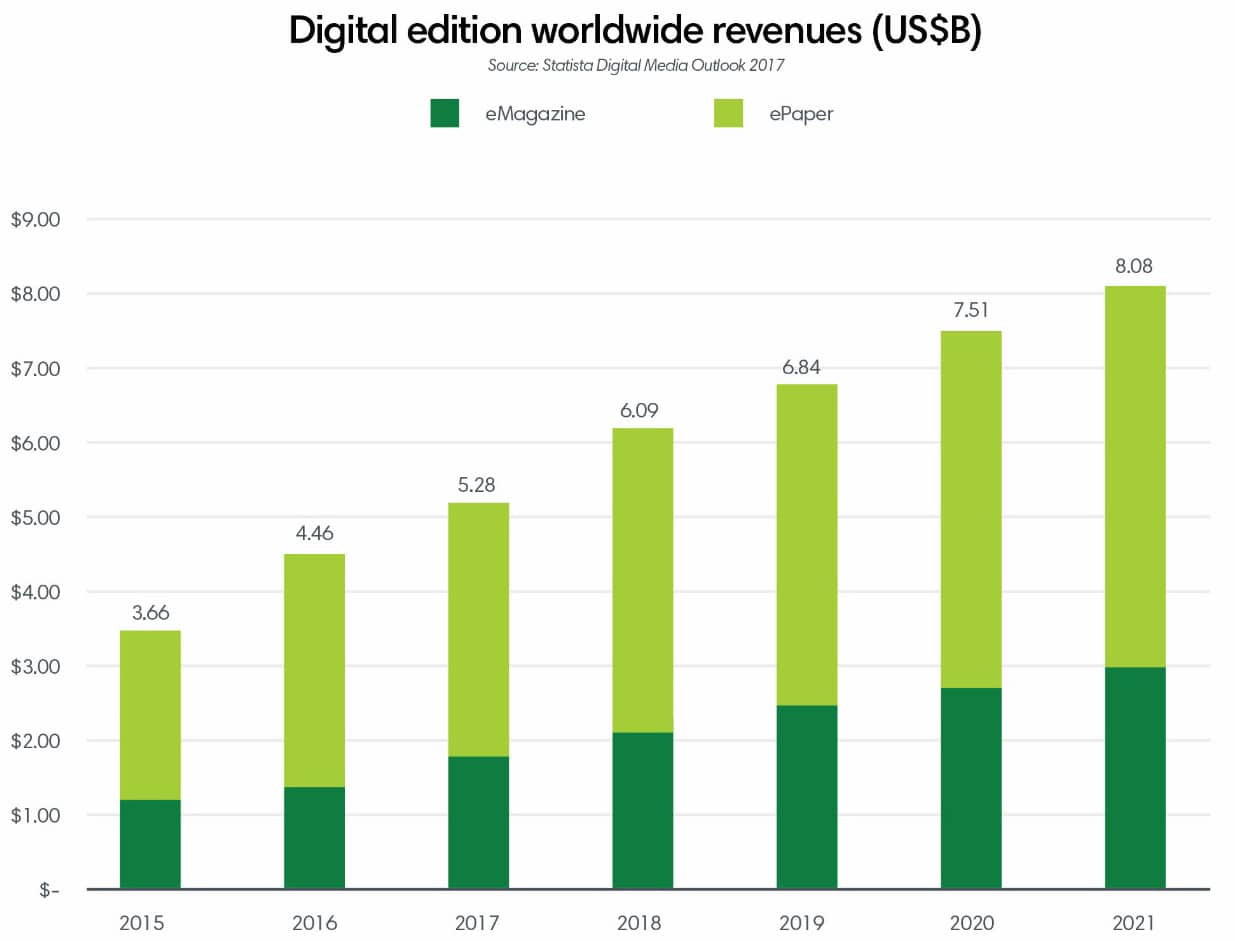

Digital edition revenue growth may not make up for losses in other areas, such as print circulation and advertising, but US$6B in revenue in 2018 is nothing to sneeze at.

Imagine how much bigger that revenue could be if more publishers actually started to build, value, and promote high quality digital editions for their most loyal subscribers. The question is, are you making it easy for them to find and read them?

Digital replica editions/ePapers may not be for everyone, but they’re definitely valued by many today and will be even more so when publishers are forced to put an end to printed publications in regions where dwindling print readership is making hard copy production and distribution unaffordable.

The Globe and Mail (G&M) faced this dilemma last year in Canada’s Maritime Provinces and made a pragmatic decision to shut down production and delivery of all printed editions in the region.

The company did, however, replace those printed issues with their very popular Globe2Go product – an audit-bureau-compliant branded edition built with award-winning technology that readers could download and read offline, with all the bells and whistles readers can’t get in print (e.g. multiple viewing options, sharing, commenting, copying, printing, embedded video viewing, instant translation, and on-demand listening).

G&M was able to automatically authenticate every print subscriber within their apps to ensure no reader was left out in the cold. And by not subsidizing print distribution, the publisher could invest more in quality content. Journalism was saved, trees were saved, and subscribers received all the content they wanted, anywhere they wanted it – online, offline, and in tablet and smartphone apps running iOS, Android, and Windows operating systems – at a lower price than the printed product. Although it was not the lower price that drove consumers to stay with the digital edition; it was the quality of the content they valued.

Digital editions are the low hanging fruit

For publishers looking to increase reader revenue, digital editions are the low hanging fruit ripe for the picking. I’ve always said that branded replicas were a niche product in a fragmented market. It’s just one of many different ways users choose to consume content, but it’s also one of the few ways that actually generates reader revenue.

Digital editions’ audience potential

According to a report published by the American Press Institute (API) in December 2017, the way people consume content is a function of “behavior, attitudes, and beliefs – not demographics.” API’s research found that digital subscribers tend to fall one of three archetypes.

- The civically committed

These people support missions and initiatives that reflect their personal values. They have a high willingness to pay, multiple subscriptions, low price sensitivity, and high loyalty. You can’t ask for more than that!

Publishers who demonstrate a real commitment to the community and partner with civically-minded brands and institutions are on the right path to profits with this audience. Combine that with an authentic desire to connect and engage with them around their values will go a long way to securing this group’s loyalty and financial support.

- Thrifty transactors

Thrifty transactors tend to have a moderate willingness to subscribe and are more discerning about “value for money” than the civically committed. They are more selective and price sensitive as well. If you’re a publisher that appeals to their specific news topic, hobby, or interest (e.g. politics, cooking, entertainment), you will find them more invested in your publication than a general news brand.

Publishers of general news brands (of which there are far too many), have little chance of attracting and retaining the interest of this discerning audience.

To thirty transactors, general news publications offer nothing unique – nothing that demonstrates excellence in key areas of interest. It’s a “differentiate or die” scenario with these folks.

- Elusive engagers

These subscription-averse readers are the most difficult to attract and engage. They have a low willingness to pay, and often view news as a commodity or “nice to have” product. They may take advantage of a new trial, but they’ll likely abandon the site when the period expires.

Publishers can make money on this frugal, “don’t lock me in” audience, but only through diversification, including multiple business models, such sponsored access, all-you-can-read, pay-per-issue, and pay-per-article (to a lesser extent).

Digital editions evoke emotional connections with the product which carries value at a price

Printed editions of magazines and newspapers have always been seen as premium products within legacy media’s portfolio. They still bring in the most reader and advertising revenue per issue, which is why so many publishers are hesitant to abandon it. But it’s a format that is losing readership every year, particularly with audiences who want anytime, anywhere access to content.

That being said, printed media still carries with it a significant perceived value with many news readers. They may not all like the format, but they trust the content more than content from any other medium. And in the infinite stream of digital debris that infiltrates their world, printed media offers a reprieve. There’s a beginning, a middle, and an end to printed media which gives readers the luxury of being able to accomplish something – completion achievement.

And as more and more publishers move towards charging for content that was once free, bundles that include previously free content and a digital edition are recognized by readers as an added value worth paying for.

Trust, perceived quality, value, and achievement that comes with printed media carries over to digital edition replicas, along with the willingness to pay for them.

Digital editions are a trajectory for subscription-based revenue, offering not-yet-captured income potential

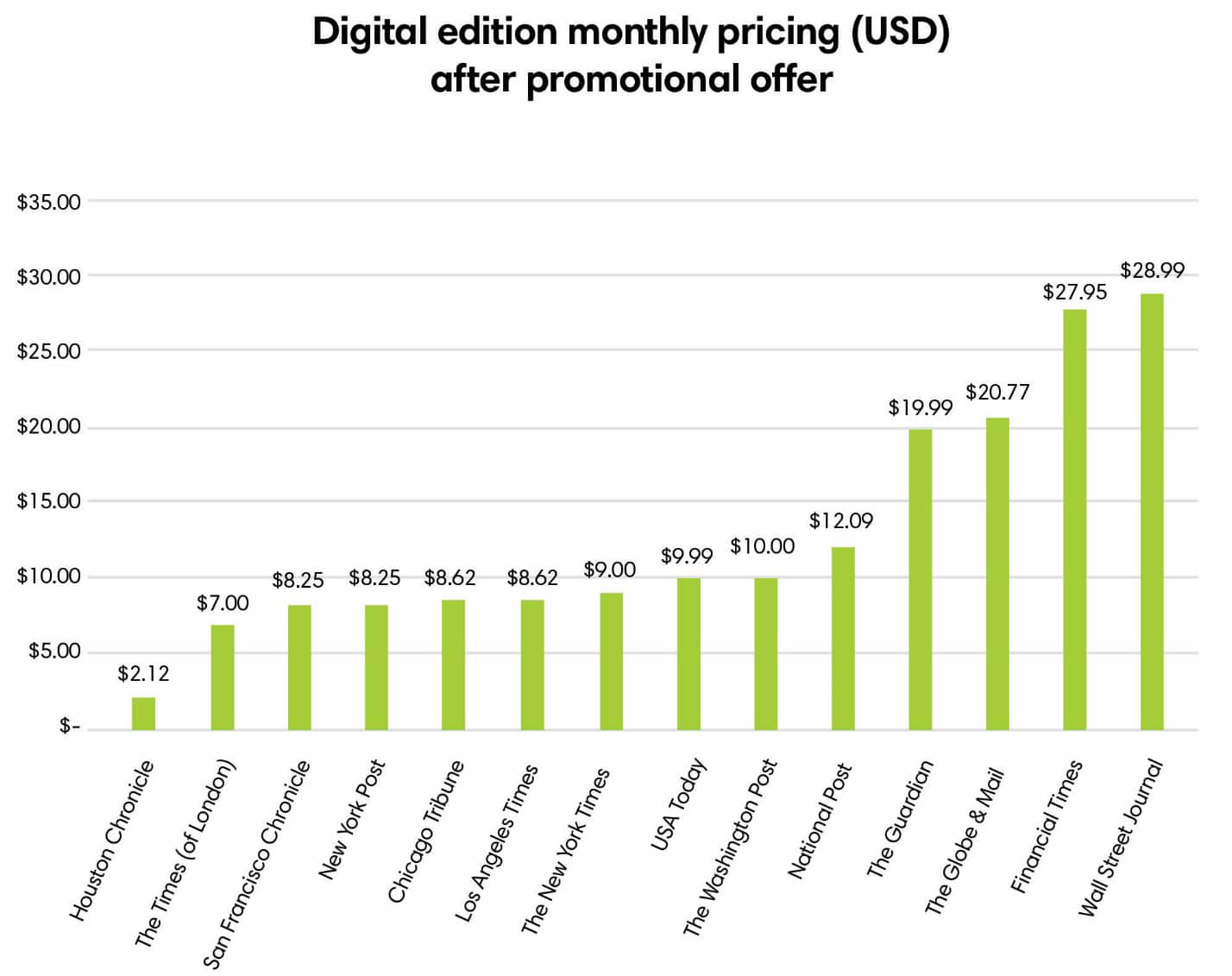

That being said, inconsistencies in pricing across markets, particularly in the US, indicate that there’s no clear standard.

The market is moving more and more towards a ‘winner take all’ scenario, where strong brands are capturing the lion’s share of subscriber revenue. Making content available in multiple platforms (app, replica app, website, print, etc.) allows for maximum engagement of a publisher’s core audience.

Digital editions offer strong potential for attracting millennial readers, despite previous market fears

A number of factors such as the Trump Bump and the overabundance of fakes news on social have brought huge opportunities for publishers, particularly in the US, and surprisingly with the elusive 18 to 34-year-old market. The number of Gen Zs (aged 18-24) who paid for digital news in 2017 rose from 4-18% and from 8-20% for Gen Ys (aged 25-34). That’s 30% of the total market!

So it would appear, that contrary to earlier assumptions, millennials do show a willingness to pay for content. And that willingness doesn’t necessarily decline as one looks at the generation following them. Other streaming services seem to have made the notion of paying for subscriptions more palatable.

“The success of digital subscription services such as Spotify, Netflix, Hulu, and Amazon Prime have normalized digital subscriptions in consumers’ minds. This, in turn, has made it possible for news publishers to make real progress in this area.”

James Hewes

President and CEO, FIPP

Earlier this year, PressReader conducted independent market research on newspaper and magazine readership in Canada and the US and learned that, when compared to people 35 and older, consumers aged 18-34:

- Value in-depth analysis more than their older counterparts

- Make more use of related stories links online

- Have a higher tendency to subscribe to multiple publications

- On average, pay the most in subscription fees on a monthly basis

Interesting, don’t you think?

The Trump Bump may be waning in some areas, but there is still an opportunity with younger readers, so don’t give up on them. They are, after all, the future of the Fourth Estate and our democracy.

Digital editions provide new opportunities for personalization and bundling

The more sophisticated your understanding of your customers, the better you’ll be able to target them with offers and content that resonate. Asking for and tracking preferences, sharing data across departments/content offerings, and testing offers with various segments will all go a long way to help optimize subscriber revenue.

Offering digital+print bundles will also make your content available in multiple ways giving subscribers what they want – the right content, in the right format, through the right channels, at, hopefully, the right price.

Control your own destiny

Digital editions offer readers and publishers many benefits, but unless people know about them, they’re like trees falling in a forest – no one will hear them when they fall and die.

By holding on to every print penny and not actively promoting their digital editions over fear of cannibalization, publishers will soon find themselves in the same sinking boat Blockbuster did when it held on tight to its DVD business, even though it had streaming technology (2002) five years before Netflix (2007). Even as late as 2009, Blockbuster executives refused to admit that its strategy was dead wrong.

“Right now, we are the leader in the rental video business in the US. To the extent that the industry moves more digital, we plan to stay the leader. We know consumers are requiring more from us and we have no wish to lose our leadership.”

Kevin Lewis

Senior VP Digital Entertainment

Blockbuster (2009)

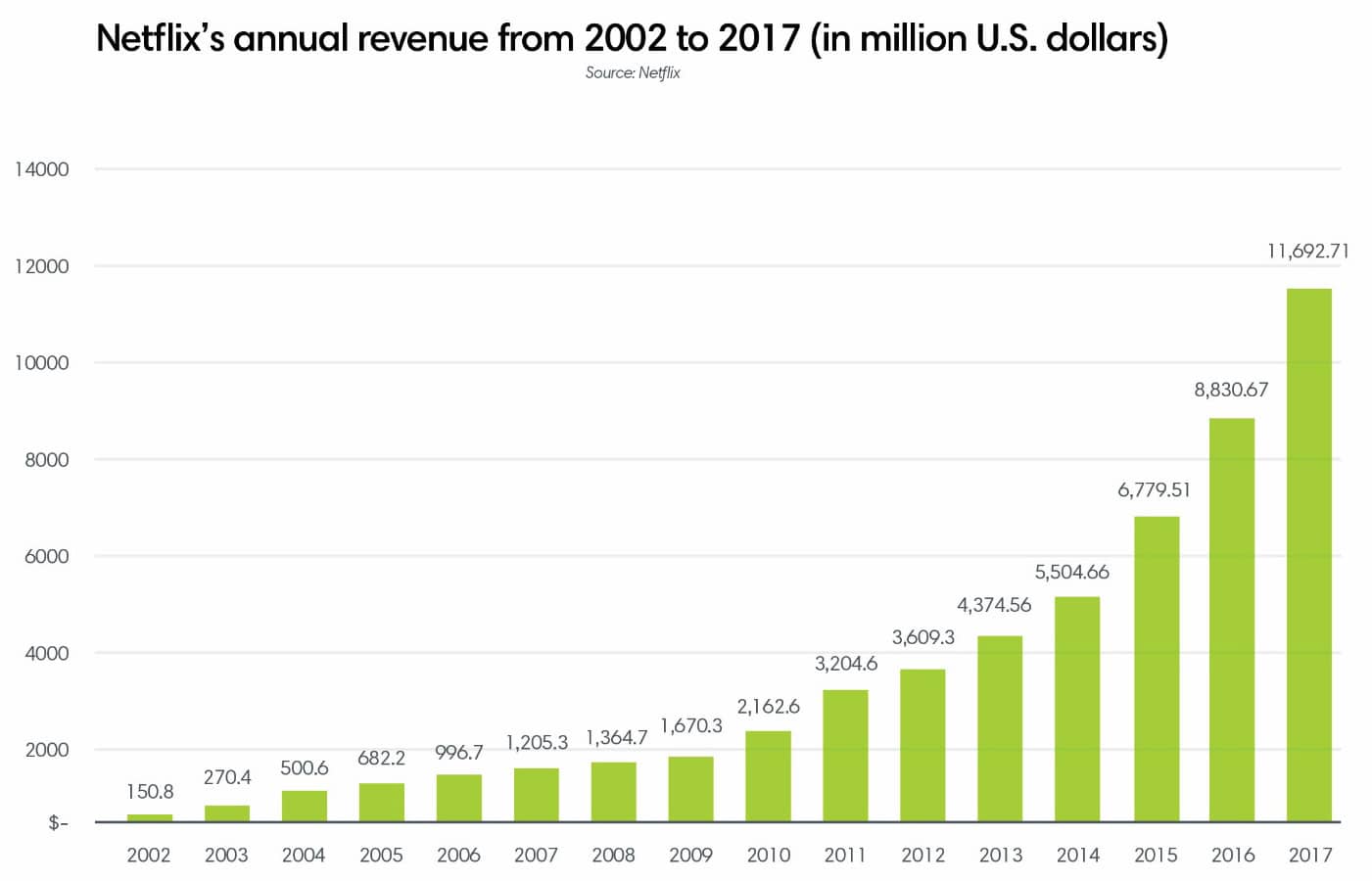

Meanwhile, Netflix actively promoted streaming, deliberately cannibalizing its own DVD business. I don’t need to tell you how that worked out. Okay, I will. 😉

In September 2010 with US$1.1B in revenue losses, and a value of only US$24M, Blockbuster filed for bankruptcy. Netflix revenues have skyrocketed to over US$11B.

It takes vision and an entrepreneurial spirit to cannibalize existing products and business models in order to pave the way for a more lucrative future. Digital editions are not an endgame; their lifespan is limited. But they are stepping stones to new digital revenues and opportunities to attract and retain brand-loyal subscribers for the foreseeable future.

Think about it. And then, let’s talk!